Most people think building an emergency fund is the hard part. It isn’t. The hard part is keeping it somewhere that actually protects you — and most people get that wrong.

A car breaks down. A medical bill lands. A job disappears with two weeks’ notice. These aren’t rare, once-in-a-decade events. They’re the normal texture of adult life, and they show up whether or not your budget is ready for them. When you don’t have cash set aside, a $1,200 repair doesn’t stay a $1,200 repair. It becomes credit card debt at 24% interest, a missed rent payment, or a 401(k) loan that quietly torches years of compounding. One bad week undoes a year of progress.

Here’s the part nobody talks about: the best place to keep emergency savings matters almost as much as having it in the first place. Park it in the wrong account and inflation eats it, you spend it by accident, or it’s locked up exactly when you need it. Park it in the right account and it sits there — safe, instantly available, and quietly earning money while it waits.

This guide breaks down exactly where to keep your emergency fund, the mistakes that quietly cost people thousands, and the specific account I use and recommend. Build in silence, let the safety net speak.

Table of Contents

- What Is an Emergency Fund?

- The Biggest Mistakes People Make With Emergency Savings

- What Makes a Good Emergency Savings Account?

- Why High-Yield Savings Accounts Are Usually the Best Choice

- Why I Recommend Marcus by Goldman Sachs

- How to Build a $10,000 Emergency Fund

- Emergency Fund vs. Investing: Which Comes First?

- A Real-Life Example

- FAQ

- Final Thoughts

What Is an Emergency Fund?

An emergency fund is a dedicated pile of cash set aside for one job: covering unexpected, necessary expenses without going into debt or selling your investments. That’s it. It’s not your vacation money, not your down payment fund, not your “I’ll invest it later” money. It’s insurance you pay yourself.

The reason every single adult needs one is simple — life is unpredictable, and predictable income meets unpredictable expenses. Without a buffer, every surprise becomes a financial emergency. With one, a surprise is just an annoyance you pay for and move on from.

The numbers show how rare this buffer actually is. According to Bankrate, nearly 1 in 4 Americans have no emergency savings at all, and 59% say they couldn’t cover an unexpected $1,000 expense from savings. Sixty percent of Americans report being uncomfortable with their level of emergency savings. This isn’t a fringe problem — it’s the default condition for most working people.

Common Emergencies People Actually Face

These aren’t hypotheticals. The most common reasons people drain their fund — or wish they had one — include:

- Job loss or reduced hours

- Medical or dental bills not fully covered by insurance

- Car repairs and unexpected vehicle costs

- Home or appliance repairs (a water heater doesn’t ask permission)

- Emergency travel for a family situation

- A sudden gap between paychecks or a delayed client payment

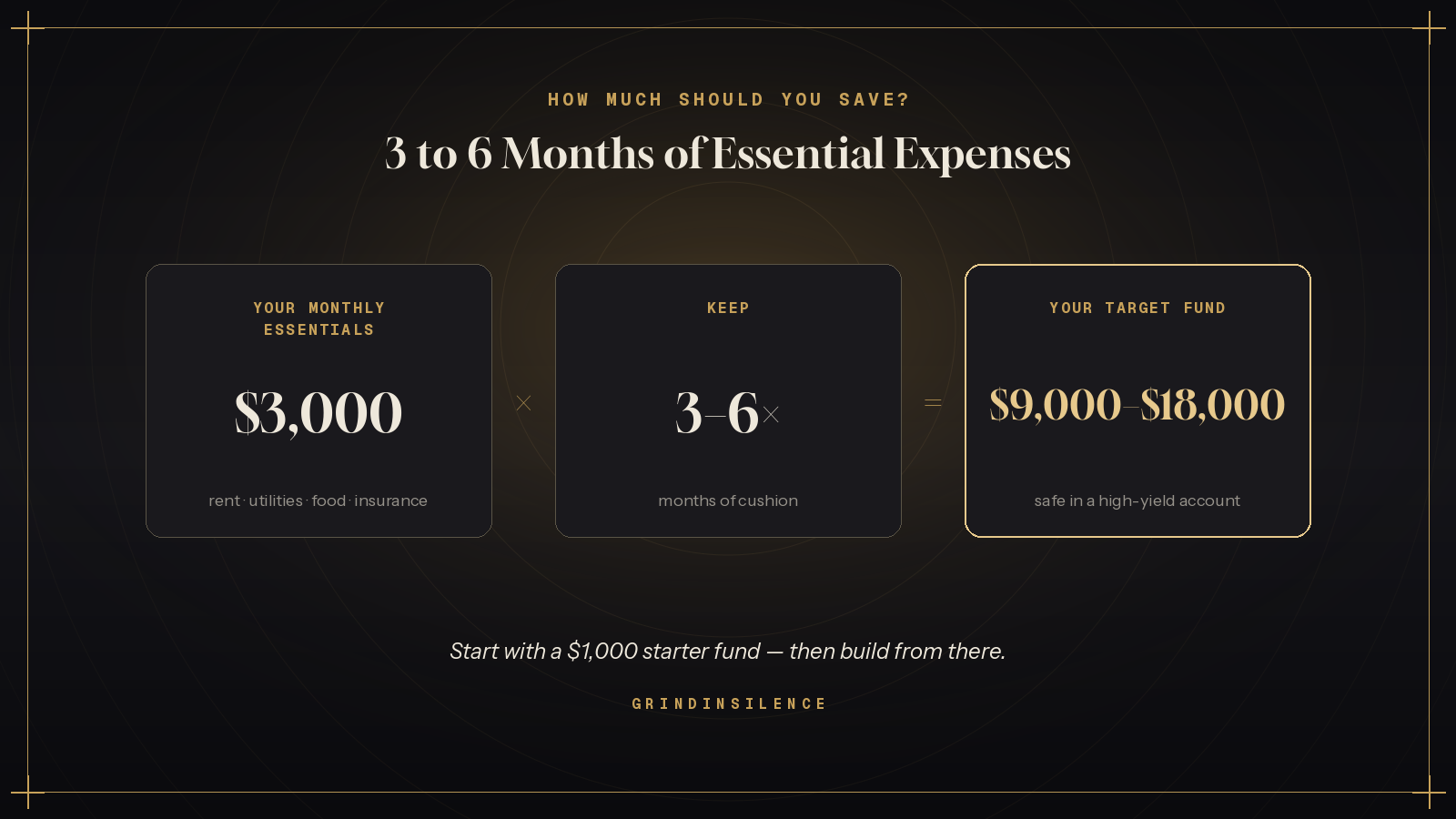

How Much Should You Save?

The standard rule is three to six months of essential living expenses. Notice the word essential — that’s rent or mortgage, utilities, groceries, insurance, minimum debt payments, and transportation. Not subscriptions, dining out, or anything you’d cut in a real crunch.

If your essential monthly costs are $3,000, your target is somewhere between $9,000 and $18,000. Start with a smaller milestone — $1,000 is the classic first goal — then build from there. If your income is variable (freelancers, commission, gig work), lean toward six months or more. Stability buys you the ability to make good decisions instead of desperate ones.

Not sure what your essential monthly costs really are? Map them out first with our free zero-based budget template.

The Biggest Mistakes People Make With Emergency Savings

Building the fund is only half the battle. Where you keep it determines whether it actually works when you need it. Here are the four mistakes that quietly cost people the most.

Mistake 1: Keeping It in Your Checking Account

This is the most common error, and it fails on two fronts. First, money sitting next to your spending money gets spent — it’s psychology, not discipline. When the line between “savings” and “available to spend” disappears, the savings disappear too.

Second, checking accounts pay essentially nothing. The FDIC national average savings rate is just 0.38% APY, and many large banks pay as little as 0.01% on deposits. Your emergency fund should at least keep pace with the world. In a checking account, it’s standing still while prices move.

Mistake 2: Investing Your Emergency Fund in Stocks

It feels smart — why let cash sit there when it could be growing in the market? Because an emergency fund’s entire purpose is to be there, in full, on your worst day. And your worst day (a layoff, a recession-driven job loss) often arrives exactly when the market is down 20%.

Investing your emergency fund means you might be forced to sell at a loss precisely when you can least afford it. Morgan Housel makes this point well in The Psychology of Money: the highest form of wealth is the ability to wake up and do what you want — and a cash cushion is what gives you room to breathe when things go wrong. Volatility and emergency cash don’t mix. Keep them in separate buckets.

Mistake 3: Hoarding Excessive Cash at Home

A small amount of physical cash for true emergencies (a power outage, a natural disaster) is reasonable. A stack of bills in a drawer as your entire fund is not. Cash at home isn’t FDIC-insured, earns zero interest, and loses purchasing power to inflation every single year. It’s also vulnerable to theft, fire, and the temptation of being a little too accessible.

Mistake 4: Treating Credit Cards as an Emergency Fund

“I’ll just put it on the card” is the most expensive plan in personal finance. A credit card isn’t savings — it’s a high-interest loan you take out at the worst possible moment. With many cards charging north of 20% APR, a $3,000 emergency can balloon into months of payments and hundreds in interest. Bankrate found that 29% of Americans now carry more credit card debt than emergency savings — a trap that compounds against you. A real fund means you face the emergency once and pay for it once.

What Makes a Good Emergency Savings Account?

If checking accounts, the stock market, your sock drawer, and credit cards are all wrong, what’s right? A good emergency savings account hits five non-negotiable criteria.

Safety

Your principal cannot be at risk. No market exposure, no chance of losing value. The money you put in is the money that’s there when you need it.

Liquidity

You need to access the cash quickly — ideally same-day or next-day. An account that locks your money for months (like many CDs) defeats the purpose. Emergencies don’t wait for a maturity date.

Accessibility

You should be able to move money out easily through a transfer or withdrawal, without jumping through hoops, but not so easily that you spend it on impulse. The sweet spot is one or two clicks away — close enough to reach in a crisis, far enough that it’s not your everyday spending account.

Interest Earnings

This is the criterion most people ignore — and it’s where the “best place” question really gets answered. Your fund will sit for months or years. It should earn a competitive return while it waits, not rot at 0.01%.

FDIC Insurance

The account must be FDIC-insured, which protects your deposits up to $250,000 per depositor, per bank, per ownership category, backed by the U.S. government. This is the line between “safe” and “hoping for the best.” Never keep your emergency fund anywhere that isn’t insured.

Why High-Yield Savings Accounts Are Usually the Best Choice

When you line those five criteria up, one type of account checks every box: the high-yield savings account (HYSA).

A high-yield savings account is exactly what it sounds like — a savings account that pays a dramatically higher interest rate than a traditional one. They’re typically offered by online banks, which skip the cost of physical branches and pass the savings to you as higher rates. They’re FDIC-insured, liquid, and accessible — they just pay you far more for the privilege of holding your money.

The Difference Is Not Small

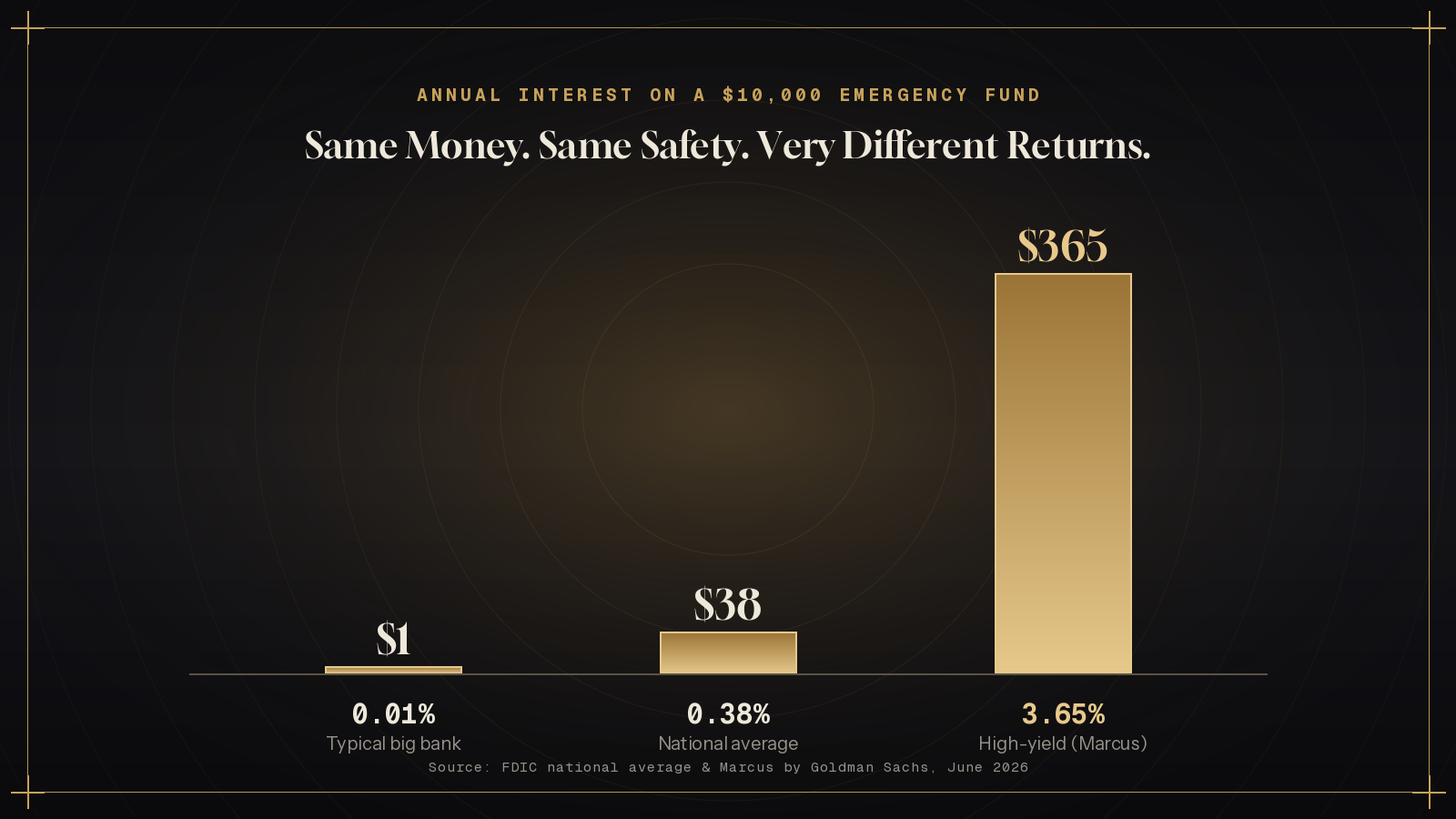

Here’s the gap that should make you act. The national average savings rate is 0.38% APY, with big-bank accounts often at 0.01%. Top high-yield savings accounts in June 2026 pay up to around 5.00% APY — roughly ten times the national average, and in some cases hundreds of times what a megabank pays.

Run the math on a $10,000 emergency fund:

- At 0.01% (typical big bank): about $1 per year.

- At 0.38% (national average): about $38 per year.

- At 3.65% (a strong HYSA): about $365 per year.

Same money. Same safety. Same instant access. The only difference is which account you chose. That’s free money you’re leaving on the table by keeping your fund in the wrong place.

Compounding and Inflation: The Quiet Forces

Most HYSAs compound interest daily or monthly, so you earn interest on your interest. Over a few years on a growing balance, that adds up to real money — and it requires nothing from you but the right account.

There’s a defensive reason too. Inflation steadily erodes the purchasing power of idle cash. Money earning 0.01% loses ground to inflation every year — it’s technically “safe” but quietly shrinking. A competitive high-yield rate helps your emergency fund hold its value over time. The Richest Man in Babylon by George S. Clason put the principle plainly nearly a century ago: make your money work for you, so that it earns even while you sleep. A HYSA is the modern, no-risk version of exactly that idea.

Want to compare your options side by side? See our full breakdown of where to keep your emergency fund.

Why I Recommend Marcus by Goldman Sachs

There are dozens of high-yield savings accounts, and honestly, several good ones. But the one I keep my own emergency fund in — and the one I recommend most often — is Marcus by Goldman Sachs. Here’s the objective case for it.

Competitive interest rate. As of June 2026, Marcus pays 3.65% APY on its Online Savings Account — variable and subject to change, but consistently far above the national average and competitive with the top tier of online banks. On a $10,000 fund, that’s roughly $365 a year for doing nothing.

No fees, no minimums. There are no monthly maintenance fees and no minimum deposit or balance required to earn the rate. You’re not penalized for keeping a modest balance or for it dipping after you use the fund. Every dollar you save earns the full rate.

FDIC insured. Marcus deposits are FDIC-insured up to $250,000 per depositor, per ownership category, backed by the full faith and credit of the U.S. government through Goldman Sachs Bank USA. Your principal is protected.

Ease of use. The platform is clean and simple — no gimmicks, no confusing tiers, no promotional-rate games that expire after three months. Setup takes minutes, transfers are straightforward, and Marcus offers 24/7 customer support by phone and chat if you ever need it.

Why it works specifically for emergency savings. Marcus hits all five criteria from the checklist above: it’s safe (FDIC-insured), liquid (transfer to your checking when you need it), accessible (but separate enough that you won’t impulse-spend it), interest-earning (a strong APY), and dead simple to manage. It’s not flashy — and that’s exactly the point. Your emergency fund should be boring, reliable, and out of sight until the day you need it.

Disclosure: If you open a Marcus account through my referral link, I may receive a referral bonus at no additional cost to you.

If you’ve been meaning to move your emergency fund out of a checking account or a 0.01% big-bank savings account, this is the simple next step. You can open an account here: Open a Marcus high-yield savings account →

Should You Split Your Emergency Fund?

For most people, one HYSA is plenty. But splitting can make sense if:

- Your fund is large (near or above the $250,000 FDIC limit at one bank) — spread it for full insurance.

- You want a small “fast-access” slice in a money market or checking buffer, with the bulk in a HYSA.

- You like keeping a little physical cash for true power-down emergencies.

Don’t overcomplicate it, though. A single high-yield savings account is the right answer for the vast majority of people.

How to Build a $10,000 Emergency Fund

Having the right account is step one. Filling it is step two. Here’s the framework I’d use to build a $10,000 fund from zero, without relying on motivation or willpower.

Step 1: Open the Right Account First

Open your high-yield savings account before you start saving. This does two things: it separates your emergency fund from your spending money, and it makes the goal real. You can’t fund a habit you haven’t set up. Five minutes now removes the biggest excuse later.

Step 2: Automate It

This is the single most important step. Set up an automatic transfer from your checking account to your HYSA the day after each payday. Even $100 per paycheck adds up — $200 a month is $2,400 a year, plus interest. When saving happens automatically, before you can spend the money, discipline stops being a daily decision. Rich Dad Poor Dad by Robert Kiyosaki drove this home for a generation: pay yourself first. Automation is how you actually do it.

Step 3: Cut Unnecessary Expenses (Temporarily)

You don’t need to live like a monk forever — just redirect spending while you build the fund. Audit your last two months of statements. Cancel the subscriptions you forgot about, pause dining out, renegotiate a bill or two. Funnel every dollar you free up straight into the fund. A focused 90-day push can move you thousands closer.

Step 4: Increase Your Income

There’s a floor on how much you can cut, but no ceiling on how much you can earn. A side hustle, freelance work, selling things you don’t use, or asking for a raise can accelerate your timeline dramatically. Dedicate extra income entirely to the fund until it’s full — then redirect it to investing.

Step 5: Track Your Progress

What gets measured gets done. Watch the balance climb toward each milestone — $1,000, then $5,000, then $10,000. Seeing progress is its own motivation, and hitting a milestone makes the next one feel inevitable. This is the GrindInSilence way: no announcements, no hype — just a number going up week after week.

Looking to boost your income? Start with these 5 side hustles you can start after work.

Emergency Fund vs. Investing: Which Comes First?

This is the question that trips up ambitious people the most. You want your money growing in the market — so why “waste” it in a savings account earning 3.65% when stocks have historically returned more? Here’s the order that actually protects your wealth.

Why Both Matter

An emergency fund and an investment portfolio do completely different jobs. The fund is defense — it keeps you from going into debt or selling assets in a crisis. Investing is offense — it builds long-term wealth. You need both, but they aren’t interchangeable, and they don’t compete for the same dollars.

Which Should Come First

The emergency fund comes first — at least a starter version. Here’s why: without a cash buffer, your first emergency forces you to either rack up high-interest debt or sell investments at a bad time. Either move can cost you more than years of market gains would have earned. The fund is the foundation that lets you invest aggressively and sleep at night.

A practical sequence: build a $1,000 starter fund, then knock out any high-interest debt, then build the fund to a full 3–6 months, and then pour everything into long-term investing. Once your fund is full, you don’t keep adding to it — you redirect that cash flow into the market.

Common Mistakes Investors Make

The two biggest errors are mirror images of each other. Some people skip the emergency fund entirely and go all-in on investing — then get wiped out by the first crisis. Others hoard far too much cash “to be safe,” leaving $50,000 earning 3.65% when it should be compounding in the market for decades. The goal is balance: enough cash to be unshakeable, and everything beyond that working hard for your future.

Once your fund is full and you are ready to grow your money, start with passive income for beginners.

A Real-Life Example

Let me make this concrete with a realistic scenario.

Picture two people, Marcus and Dana (no relation to the bank). Both earn $4,500 a month. Both are 28, ambitious, and focused on building wealth.

Dana keeps everything in one checking account. It feels efficient — one place, easy to see. There’s usually a couple thousand floating in there, but it gets spent down most months. No separate emergency fund.

Marcus keeps three months of essential expenses — about $9,000 — in a high-yield savings account earning 3.65%. It’s separate from his checking, automated, and out of sight. It quietly earns him around $330 a year.

Then the same thing happens to both of them: a layoff. Severance is thin, and it takes them each about ten weeks to land the next role.

Dana’s ten weeks are brutal. Rent and bills don’t stop. Within three weeks the checking account is empty, so the credit cards come out — groceries, the car payment, utilities. By the time a new job starts, Dana is carrying about $6,500 in credit card debt at 24% APR. Paying it off takes the next 14 months and costs over $900 in interest. The layoff didn’t just cost ten weeks of income; it set Dana’s financial progress back more than a year.

Marcus’s ten weeks are stressful but stable. He taps the emergency fund for rent, groceries, and bills. He job-hunts from a position of calm instead of panic — he can wait for the right offer instead of grabbing the first desperate one. When the new job starts, he spends the next few months refilling the fund. No debt. No interest. No setback. The emergency didn’t derail him; the system he built absorbed it.

Same income. Same emergency. Two completely different outcomes — decided entirely by whether the money was in the right place before the storm hit. That’s the whole point. You don’t build an emergency fund for the version of you who’s doing fine. You build it for the version of you having the worst week of the year.

FAQ

What is the best place to keep emergency savings?

For most people, the best place to keep emergency savings is a high-yield savings account (HYSA) at an FDIC-insured bank. It keeps your money safe, liquid, and instantly accessible while earning a competitive interest rate — often around 10 times the national average. It separates the fund from your everyday spending so you won’t accidentally drain it.

How much should I keep in my emergency fund?

Aim for three to six months of essential living expenses — rent, utilities, groceries, insurance, transportation, and minimum debt payments. Start with a $1,000 starter fund, then build toward the full amount. If your income is variable or you support a family, lean toward six months or more.

Should I keep my emergency fund in checking or savings?

Savings — specifically a high-yield savings account. Checking accounts pay almost no interest (often 0.01%), and keeping the fund alongside your spending money makes it far more likely you’ll spend it. A separate high-yield savings account keeps it earning and protected from impulse spending.

Is a high-yield savings account safe?

Yes, as long as it’s at an FDIC-insured institution. FDIC insurance protects your deposits up to $250,000 per depositor, per bank, per ownership category, backed by the U.S. government. Your principal does not fluctuate with the market, so there’s no risk of losing value the way there is with stocks.

Can I lose money in a high-yield savings account?

You can’t lose your principal in an FDIC-insured account up to the insured limits. The interest rate is variable, so your APY can rise or fall over time, but your balance won’t drop because of market movements. The only real “loss” is purchasing power if your rate falls below inflation — which is exactly why a competitive HYSA beats a 0.01% account.

Should I invest my emergency fund instead?

No. The purpose of an emergency fund is to be fully available on your worst day, which often coincides with a market downturn. Investing it risks being forced to sell at a loss exactly when you need the cash. Keep your emergency fund in a safe, liquid account and invest separately once the fund is full.

How long does it take to access money in a high-yield savings account?

Usually one to three business days to transfer to your linked checking account, and sometimes same-day. That’s fast enough for nearly every real emergency, while still being separate enough that you won’t spend it impulsively. For true same-minute needs, keep a small buffer in checking.

Why is Marcus by Goldman Sachs a good place for emergency savings?

Marcus by Goldman Sachs offers a competitive APY (3.65% as of June 2026), no monthly fees, no minimum balance, FDIC insurance up to $250,000, and 24/7 customer support. It’s simple to use and keeps your fund separate from daily spending — checking every box an emergency savings account should.

Final Thoughts: Security Is the Foundation of Freedom

Building wealth isn’t about one brilliant move. It’s about not getting knocked off the board — staying in the game long enough for discipline and compounding to do their work. Your emergency fund is what keeps you on the board.

The discipline here is quiet and unglamorous. Nobody posts about their high-yield savings balance. There’s no thrill in watching cash sit safely in an account. But that boring, disciplined cushion is what lets you take real risks elsewhere — start the business, leave the toxic job, invest through a downturn — because you know your floor won’t give out. Financial security isn’t the opposite of ambition. It’s the launchpad for it.

Think long-term. The version of you twelve months from now will either be grateful you set this up or wish you had. The unexpected expense is coming — it always does. The only question is whether it finds you ready.

So here’s your move today: open a high-yield savings account, automate a transfer, and start building. Even $50 this week is a start. You can open a Marcus high-yield savings account here →

Build the floor. Then go build everything else. Build in silence — let the safety net speak when it matters.

Featured Image Recommendation

A clean, modern flat-lay or conceptual image of a protective shield or umbrella over a stack of coins / a savings jar, in GrindInSilence brand colors. Should convey protection + growth, not stress. Alt text: “The best place to keep emergency savings — a safe, high-yield account.”

About Felix Guzman

Felix Guzman is a personal finance writer and the founder of Grind In Silence. He writes about money mindset, wealth building, and escaping the paycheck-to-paycheck cycle — with no fluff and no get-rich-quick promises. His mission: help everyday people build real, lasting wealth by making smarter financial decisions every day.